{kind=link}

Life insurance companies are financial institutions that provide insurance policies to protect individuals and families against financial loss caused by death or certain life events. In exchange for regular premium payments, the company promises to pay a sum of money (death benefit) to the beneficiary if the insured person dies during the policy period or after maturity.

Table of Contents

What Is Life Insurance?

It is a contract between an individual and an insurance company where the insurer provides financial protection and savings benefits in return for premiums paid by the policyholder.

Why do life insurance companies invest in premiums?

This companies assure financial security to their clients in case of unexpected events, i.e. death, disability or illness. In order to achieve this, they must be in a position to finance the claims and benefits of their policyholders, and their operational costs and expenses.

However, the life insurance policy premiums they collect from their customers are insufficient to meet these obligations. That is because, is a long-term contract, and the claims and benefits may occur many years after the premiums are paid. Moreover, the premiums are usually fixed and do not increase with inflation or the rising cost of living.

Main Functions of Life Insurance Companies

| Function | Description |

| Risk Protection | Provides financial support to beneficiaries if the insured person dies during the policy period. |

| Financial Security for Families | Ensures that dependents can maintain their standard of living after the policyholder’s death. |

| Long-Term Savings | Some policies help individuals build savings over time through regular premium payments. |

| Investment Management | Insurance companies invest collected premiums in bonds, stocks, and other assets to generate returns. |

| Retirement Planning | Certain policies provide income or lump-sum benefits during retirement. |

| Wealth Transfer | Helps transfer wealth to heirs or beneficiaries efficiently. |

| Loan Facility | Many life insurance policies allow policyholders to take loans against the policy value. |

| Tax Benefits | Premium payments and maturity benefits may qualify for tax advantages depending on regulations. |

| Economic Development | Insurance companies invest funds in infrastructure, government securities, and businesses, supporting economic growth. |

| Risk Pooling | Collect premiums from many policyholders to spread and manage financial risks effectively. |

Benefits of Investing Premiums

- Life insurance companies must invest their premiums to generate additional income and grow their funds. By investing in premiums, they can ensure that they have enough money to pay their policyholders’ future claims and benefits and earn profits for their shareholders and stakeholders.

- Investing the life insurance premiums also helps life insurance companies to manage their risks and liabilities. For example, if the mortality rate of their policyholders is higher than expected, they may face more claims and benefits than anticipated. They can hedge against this risk by investing in premiums and reducing their losses.

- Investing in premiums also benefits the policyholders, as it allows life insurance companies to offer more competitive and attractive products and services. For example, some life insurance products, such as unit-linked insurance plans (ULIPs) or guaranteed return plans, offer a share of the investment returns to the policyholders in addition to the policy coverage. This way, the policyholders can enjoy both protection and wealth creation from their life insurance policy.

Key Features of Life Insurance Investment Plans

| Feature | Description |

| Life Cover | Provides financial protection to the nominee in case of the policyholder’s death. |

| Savings Component | A portion of the premium is invested to grow wealth. |

| Tax Benefits | Premiums may qualify for tax deductions under applicable tax laws. |

| Flexible Investment Options | Some plans allow switching between equity and debt funds. |

| Long-Term Wealth Creation | Ideal for building funds for future goals. |

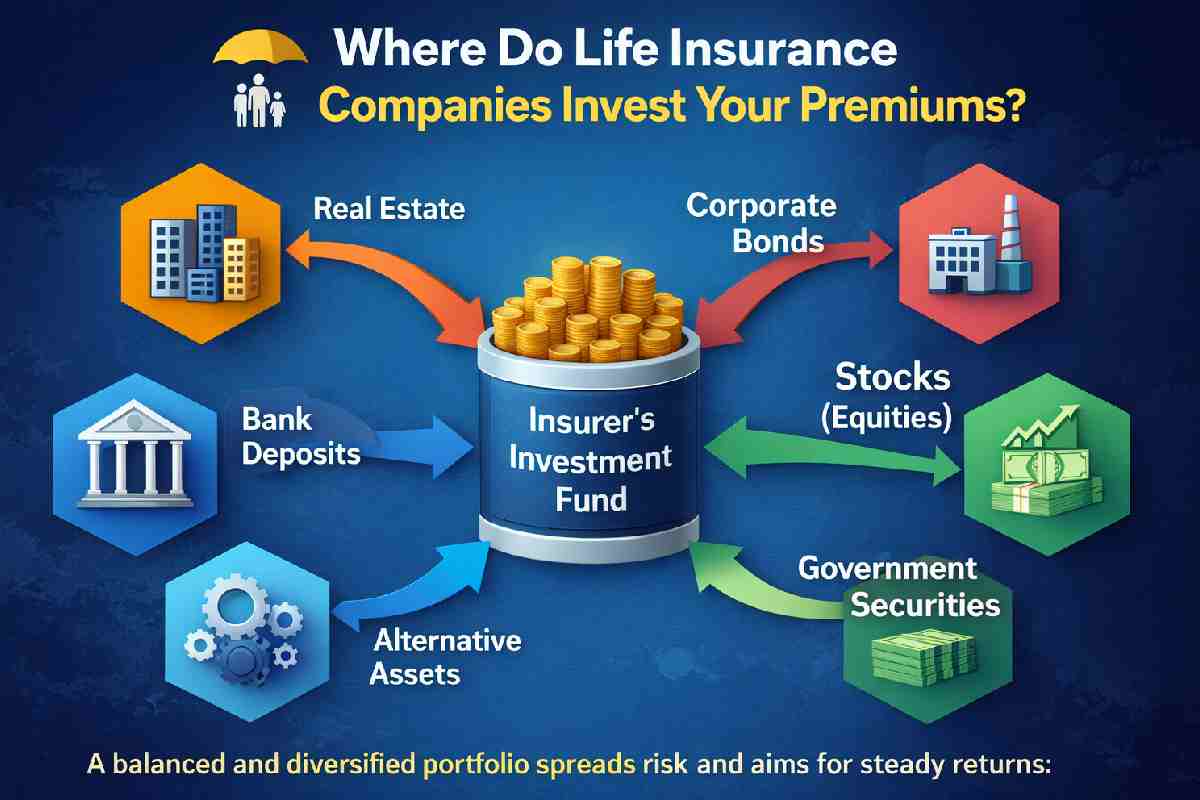

Where Do Life Insurance Companies Invest Premiums?

Life insurance companies collect premiums from policyholders and invest that money to generate returns. These investments help insurers pay future claims, bonuses, and operational costs while keeping the company financially stable.

Government Bonds

Life insurers invest a large portion of premiums in government securities because they are considered very safe and stable.

Why they invest here:

- Low risk

- Guaranteed interest returns

- Long-term maturity matches insurance liabilities

Examples:

- Treasury bonds

- Government securities (G-secs)

Corporate Bonds

Insurance companies also invest in corporate bonds issued by large companies.

Benefits:

- Higher interest rates than government bonds

- Relatively stable income

- Long-term investment opportunities

Stocks (Equities)

Some premiums are invested in the stock market to generate higher returns over time.

Advantages:

- Potential for long-term capital growth

- Dividend income

- Portfolio diversification

However, equity investments carry higher risk compared to bonds.

Real Estate

Insurance companies invest in commercial properties and infrastructure projects.

Examples:

- Office buildings

- Shopping malls

- Infrastructure developments

Benefits:

- Rental income

- Long-term asset appreciation

Money Market Instruments

For short-term liquidity, insurers invest in money market instruments.

Examples:

- Treasury bills

- Commercial paper

- Certificates of deposit

Purpose:

- Maintain cash flow

- Pay claims quickly when needed

| Investment Type | Risk Level | Purpose |

| Government Bonds | Very Low | Stable long-term returns |

| Corporate Bonds | Low–Medium | Higher interest income |

| Stocks | Medium–High | Growth and dividends |

| Real Estate | Medium | Rental income and appreciation |

| Money Market Instruments | Low | Short-term liquidity |

Types of Life Insurance Policies

It policies come in different forms to meet various financial needs such as family protection, savings, investment, and retirement planning. Below are the most common types.

- Term Life Insurance

It provides coverage for a specific period, such as 10, 20, or 30 years.

Key features:

- Low premiums

- High coverage amount

- No maturity benefit (unless specified)

Best for: Financial protection for family during earning years.

- Whole Life Insurance

It offers lifetime coverage along with a cash value component that grows over time.

Key features:

- Coverage for entire life

- Savings or investment component

- Higher premiums compared to term insurance

Best for: Long-term financial security and wealth planning.

- Endowment Plans

An endowment plan combines life insurance protection with savings.

Key features:

- Lump sum payout at maturity or death

- Helps build long-term savings

- Lower risk investment option

Best for: People looking for both protection and savings.

- Unit-Linked Insurance Plans (ULIPs)

ULIPs combine life insurance with market-linked investments.

Key features:

- Part of the premium invested in equity or debt funds

- Potential for higher returns

- Market risk involved

Best for: Investors who want insurance plus investment growth.

- Money-Back Policy

A money-back policy provides periodic payments during the policy term.

Key features:

- Regular payouts during policy duration

- Death benefit protection

- Suitable for planned expenses

Best for: People who need periodic financial returns.

Best life insurance investment plan

A investment plan combines financial protection (life cover) with wealth creation or savings. These plans help secure your family financially while also building a fund for future goals such as retirement, children’s education, or wealth growth.

Below is a comparison table of some popular types of life insurance investment plans to help understand which option may suit different financial goals.

| Plan Type | Investment Feature | Risk Level | Returns Potential | Lock-in Period | Best For |

| ULIP (Unit Linked Insurance Plan) | Invests in equity, debt, or hybrid funds | High to Medium | Market-linked (potentially high) | 5 years | Long-term wealth creation |

| Endowment Plan | Fixed savings with insurance coverage | Low | Guaranteed returns | 10–20 years | Safe long-term savings |

| Money Back Plan | Periodic payouts during policy term | Low | Moderate | 15–25 years | Regular income along with insurance |

| Whole Life Insurance Plan | Lifetime coverage with savings component | Low to Medium | Moderate | Lifetime | Estate planning and legacy |

| Retirement / Pension Plan | Builds retirement corpus | Medium | Market-linked or fixed | Until retirement age | Retirement planning |

| Child Investment Plan | Savings plan for child’s future | Medium | Moderate to high | Long-term (10–20 years) | Child education & marriage goals |

Major Life Insurance Companies (Global Examples)

| Company | Country | Founded | Key Highlights |

| Allianz | Germany | 1890 | One of the world’s largest insurers offering life, health, and asset management services. |

| MetLife | United States | 1868 | A leading global provider of life insurance, annuities, and employee benefits. |

| Prudential plc | United Kingdom | 1848 | Major life insurer with strong presence in Asia and Africa. |

| AIA Group | Hong Kong | 1919 | One of the largest life insurance companies in Asia-Pacific. |

| AXA | France | 1816 | Provides insurance, investment management, and financial services worldwide. |

| Ping An Insurance | China | 1988 | One of the biggest insurers globally with strong technology-driven services. |

| Life Insurance Corporation of India | India | 1956 | Largest life insurance provider in India with millions of policyholders. |

| Manulife | Canada | 1887 | Offers life insurance and financial services across Asia and North America. |

Conclusion

The prudent investment of premiums is integral to the functioning of life insurance companies. Through strategic allocation across diverse assets, such as bonds and equities, insurers aim to ensure financial stability, meet future obligations, and offer competitive products. Understanding this investment landscape sheds light on the symbiotic relationship between policyholders, insurers, and the dynamic financial markets.